When the first wave of the COVID-19 pandemic brought the world to a grim standstill back in March 2020, 28-year-old Kallie Vangas’s life was among the many turned upside down after being infected. Day by day, Vangas’s case shifted from the usual fever and chills to more persistent problems like labored breathing and increased heart rate. For the first few months, her constant pleas from doctors were shrugged off as anxiety, even as her issues grew in frequency and ferocity.

“I struggled with shortness of breath, where I was physically gasping for air on my bed for five months straight holding my diaphragm, just trying to push air into my lungs so I could breathe,” says Vangas, who lives in Nyack. “I was pretty much gaslighted from the beginning…They didn’t know anything about the virus at the time, so it’s kind of unfair, but that’s what they did.”

After numerous specialist visits during a beleaguered year, Vangas is managing to adjust to her new life as one of the hundreds of thousands of long COVID sufferers whose initial bouts with the virus put them in a state of medical limbo, with chronic health issues that have doctors and researchers stumped. A fitness enthusiast who formerly could be found on a hiking trail or in the gym with her fiancé, Vangas now has difficulty completing day-to-day tasks.

“Taking a shower is exhausting,” she says. “There’s times where I can’t drive and I have to literally tell my parents, ‘You have to take me to my doctor’s appointment because if I drive, I might get into a car accident’—the brain fog gets so bad that you can’t focus.”

But a bout with COVID-19 can be as challenging financially as it is physically. The federal CARES Act created a Provider Relief Fund to help waive the costs of COVID-related testing and treatment, but very few have had luck with it, since it relies on positive PCR tests, which were hard to come by early in the pandemic. That leaves people unfortunate enough to fall ill with the virus in a bind as to how to support themselves through the recovery process.

For Vangas, the journey toward healing has been wrought with pain. For a little while, as her doctors bounced back and forth between possible answers, she was able to make it work financially thanks to the health insurance and FMLA benefits provided by her job. However, the weeks spent unable to work didn’t fly with her insurance company, causing lapses in her coverage. Once Vangas’s relationship with her fiancé buckled under the stress, she lost out on another potential source of coverage. In less than a year, she had joined the ranks of thousands of other COVID patients who struggle to find respite because they’re either underinsured or uninsured.

This is a problem designed to be solved by the New York Health Act. First introduced back in 1992, the bill sets out to establish a single-payer solution to health care, where the state would act as the sole insurer for nearly 20 million New Yorkers. In the aftermath of a once-in-a-century pandemic, advocates feel that providing guaranteed health coverage has never been more urgent.

A Club No One Wants to Join

The financial troubles experienced by Vangas have become increasingly common during the economic fallout of the pandemic. The most conservative estimates have over two million Americans losing their employer-provided health coverage between March and September last year, and that was after a period starting in 2017 where almost 3 million lost insurance due to declines in Medicaid and non-group coverage. With the medical establishment still reeling and hospital bills piling up, many have resorted to crowdfunding to make ends meet, sharing advice in online forums like the 12,000-strong COVID-19 Long-Haulers Discussion Group.

“People are fighting tooth and nail,” Amanda Finley, founder of the Facebook group and a long COVID patient, says. “There are a lot of people in the group [with jobs and insurance] who have thousands upon thousands in medical bills. And then there are some people who did lose their job and their insurance.” Finley launched the group in June 2020 after contracting and battling the virus in March of that year. Since then, she’s heard hundreds of stories similar to hers: a healthy, productive person beat down by COVID and left with fatigue, heart palpitations, and other debilitating symptoms, on top of crushing medical debt.

“Even when we had tests three weeks later in Kansas City, I still didn’t qualify because my temperature never peaked over 100.4,” Finley says. “I knew I couldn’t afford a chest CT and all of those things, so I just rode it out at home.” Although Finley is on Medicaid now, she still dreads the time when she waited out a potential heart attack to avoid a pricey trip to the hospital.

On the federal level, recent incentives tucked away in the American Rescue Plan are aimed at alleviating the gaps in coverage by building on the provisions established within the Affordable Care Act and Medicaid. In the past few years, similar initiatives have helped New York reach a record low uninsured rate of 4.7 percent, compared to 10.9 percent nationwide, but they’ve done little to quell the exorbitant costs (insurance premiums, copays, and deductibles) New Yorkers pay compared to the national average, which clocks in at $1,000 more per person according to a 2019 report by the New York State Health Foundation. As lawmakers squabble over the regulations, or lack of, that have contributed to the problem, others think it’s time to do away with the current system entirely.

A New System for a New Normal

Within the confines of the state Legislature, a majority of lawmakers in both the state Assembly and Senate have signed on as sponsors of Assembly Bill A6058, more commonly referred to as the New York Health Act. From the sleepy mountain towns of the Adirondacks to the brash McMansions out in the Hamptons, supporters promise a system that would provide comprehensive medical care to all (including dental, vision, and long-term care) by having all medical providers operating within the Empire State under one massive network.

“This is about guaranteeing health care, and anybody who has insurance can tell you about the fact that just having an insurance card in your pocket does not guarantee you care in any way, shape, or form,” says state Senator Gustavo Rivera (D-Bronx), the Senate sponsor of the bill.

Supporters of the New York Health Act are well positioned for an assist from the federal government: the chances of receiving the waivers necessary to use ACA and Medicaid funds for the NYHA are better than ever, with noted single-payer advocate Xavier Becerra serving as President Biden’s secretary of health and human services. Aside from the contributions within their own budgets, each state relies on the federal government for funds to bolster marketplace plans and public programs. Medicaid spending in New York State continues to increase in concert with rising enrollment and the latest influx of federal stimulus aid; total spending this year is expected to hit $80.3 billion, $4.5 billion more than in 2020. Federal waivers would let New York use those funds to prop up the NYHA, putting the pricey patient base covered under those plans under the auspices of the newly formed single-payer state plan. And with a solid Democratic supermajority in the state Senate since 2019, the sixth time might be the charm in getting it passed in both chambers.

But not everyone is sold yet. Depending on whom you speak to, the idea of a single-payer system anywhere in the United States sparks equal amounts of curiosity and skepticism. Even though the most modest polls have more than half of the country supporting Medicare-for-all, detractors are quick to conjure up scenarios where the government has complete control over what doctor you can see and when, with little personal choice. Diehard promoters of single-payer health care, like NYHA architect Assemblymember Richard Gottfried (D-Manhattan), believe that getting rid of the current system of insurers, networks, and premiums is the only real path to freedom of choice for patients. They posit that having all New Yorkers—rich and poor, Black and white—covered under the same plan ensures that no one would lose out on receiving the best care for lack of funds.

“The insurance industry likes to say, ‘Nobody wants the government telling your doctor what to do. Nobody wants a one-size-fits all healthcare system,’” Assemblymember Gottfried says. “That's all true. And that’s part of why nobody wants an insurance company telling them what doctor they can go to, or telling their doctor what care to provide. The New York Health Act doesn’t say one size fits all. It says, ‘We’re not going to have sizes.’”

The devastation brought on by the pandemic has raised the profile of big, bold initiatives like the New York Health Act. As politicians and professionals ponder over the policies that’ll shape whatever the new normal looks like, there have been renewed calls for some form of universal health care to be part of the solution. A February 2021 report published by the medical journal The Lancet concluded that 40 percent of the then-450,000 COVID-19 deaths in the US were preventable; one of the report’s recommendations includes establishing a national single-payer health insurance system similar to those in Canada or the UK. The benefit of no medical costs could encourage people to get early testing and treatment before an illness gets out of control, COVID or otherwise. Moreover, the current labyrinth of paperwork and phone calls that accompany appealing a denied claim can wear down even the most astute people.

“A lot of the symptoms that go along with having long COVID involve brain fog and mental fatigue,” Finley says. “You can’t think straight. So here you got this stack of bills and you don’t even know where to start. It’s very daunting.”

The most recent economic assessment of the bill, the 2018 RAND Corporation study, predicts total healthcare spending under the NYHA to clock in at $309 billion in 2022, compared to $311 billion under the current system, with cumulative net savings of around $80 billion over the next decade. In the eyes of Gottfried, Rivera, and company, the prospect of covering around a million uninsured New Yorkers for comparable costs in the present reads like a bargain.

Arguments against the NYHA

Critics, on the other hand, see the deluge of new patients and increased healthcare expenditures as a potential bottleneck for medical providers. The most apprehensive and vocal among them—such as Bill Hammond, the senior health policy fellow at the Empire Center for Public Policy—balk at the idea of putting the onus on the state government to cover citizens, especially when the current administration had previously been open to the idea of cuts to the public health system to balance the budget.

“Even if you take for granted that the new system can cover more people and more benefits with fewer restraints at roughly the same cost as the status quo, which is dubious in the extreme, this proposal would put the entire $300 billion health system on New York’s balance sheet—making the rest of state government look small by comparison,” Hammond said in an interview with Gothamist back in March.

Opponents’ fears are exacerbated by the proposal’s inclusion of long-term-care coverage, which knocks the total price up a notch, and the confusing language regarding out-of-state commuters employed in the state. For them, upending the current marketplace of insurers seems counterintuitive, given that millions have enrolled in these plans during the pandemic. They warn that a disruption of that scale would be too big and happen too fast for there not to be long-lasting damage.

“Savings under the NYHA rely on reduced rates to doctors, hospitals, and other providers,” says Leanne Politi, executive director of Communications for the Realities of Single Payer, a coalition of groups opposed to the New York Health Act. “The majority of hospitals would see funding cuts on day one of implementation. Lower payments would force providers to make cuts somewhere, whether it’s to services or staff.” The RAND study points out that the 40 percent drop in health plan administrative costs would offset the increased spending and use, and that’s alongside what proponents say would be a lucrative environment for doctors to treat more patients than they could have before without having to worry if they’re insured or not.

A major selling point touted by single-payer advocates is the promise that patients and doctors alike wouldn’t be beholden to the financial whims of insurance companies. With savings top of mind, they argue that insurance companies view those with persistent health problems as too costly to care for; in fact, a 2018 nationwide survey commissioned by the Doctor-Patient Rights Project found a 24 percent denial rate in claims from those suffering chronic illnesses. In Vangas’s case, there were a few instances where her insurance tried to deny her claims for monthly blood work or a new MRI.

“Come January of this year, my primary care doctor who’s been dealing with this problem with me went out of network with my insurance,” she says. “So I was forced to find a new doctor, or else I would’ve been billed out of the ass, but they don’t know my entire history of what’s been happening to me.”

To further complicate matters, ICD-10-CM (International Classification of Diseases) codes—the system used by providers to identify illness and bill insurers—may lack the specificity needed for a complete provider transition. Some patient advocates and physicians argue that the current set of new ICD-10-CM codes for COVID, which went into effect on January 1, do little to express the full breadth of symptoms experienced by long COVID sufferers—up to 170 shared by at least a dozen people in some cases—and could allow insurers to limit the scope of care. These limitations were nothing new for people with complex conditions before the pandemic.

“In contrast, my experience has been one of doctors who don’t know what to do with me. Misdiagnoses were common, especially in the early years of my illness,” says Lynn Esteban. Back in January, the Poughkeepsie resident and NYHA supporter penned a poignant letter to the state Senate detailing her years long battle with myalgic encephalomyelitis (chronic fatigue syndrome) and how her husband’s insurance muddled things by delaying her IV drug treatment regimen.

“When I finally did get an accurate diagnosis and tests that revealed a potential treatment, the doctor couldn’t prescribe the treatment because he’s out of state,” Esteban says. “I then had to seek out a new neurologist in New York. The treatment was automatically denied, then there was a long appeal process that went on for several months.”

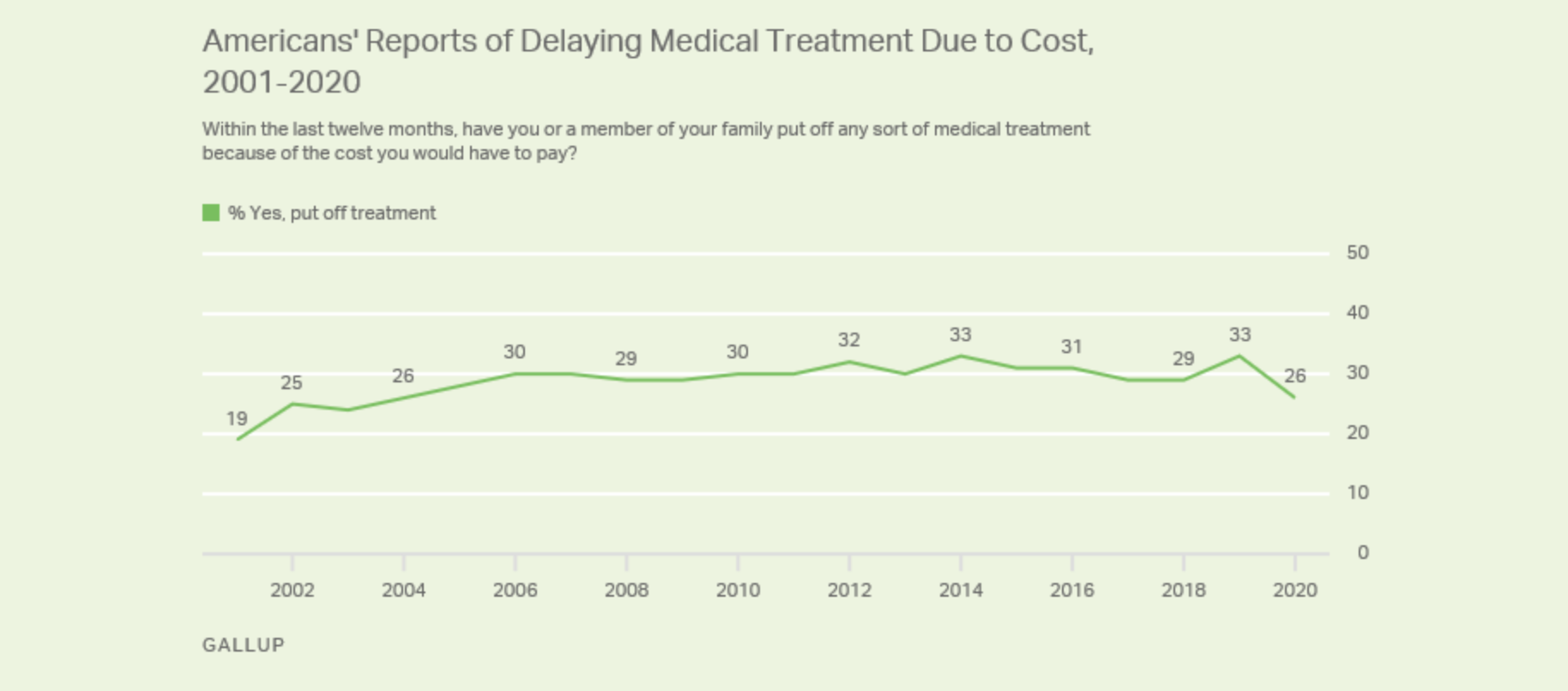

It’s these imperfections that make skeptics of single-payer assert that New Yorkers would still face lengthy wait times for certain specialists and noncritical care, the classic example being lengthy holdups for knee and hip replacements in Canada. For some referrals and treatments in Canada, wait times can be long, particularly in rural areas, but that could be attributed to a concentrated supply of doctors tasked with treating the country’s thinly-spread population. In the US, however, delays in care due to high costs remain common; about a quarter of Americans still put off treatment because of the price tag, even as healthcare satisfaction hit a 20-year high at 67 percent, according to a December 2020 Gallup poll.

“They may tolerate it, but nobody loves their health plan,” Gottfried says. “I always think that it’s kind of like if you’re on an ocean liner and it sinks—you love your life, but it’s not where you want to be in the North Atlantic in winter.”

What Now?

As it stands, the New York Health Act is winding its way through the state Legislature. On April 19, the Assembly Health Committee voted to pass it, sending it over to the Ways and Means and Codes committees for further approval before it is potentially brought to the floor for a vote.

Over the last three decades, NYHA organizers like the Campaign for New York Health have put together an impressive coalition of allies, including the eastern division of the 1199SEIU healthcare workers union, the New York State Nurses Association, the New York State Academy of Family Physicians, and many others. The greatest opposition to overcome might be from well-off New Yorkers who would see the highest taxes under the gradual income tax rates (including interests, dividends, and capital gains) that are called for to fund a fifth of the program’s $139 billion price tag. Under the RAND study’s proposed tax brackets, the savings per person would be nonexistent for the wealthiest, with the top 5 percent of earners (those making $1,255,700 a year and more) actually spending more for care ($50,200 per person compared to around $44,800 per person). At a time when Governor Cuomo has been apprehensive about raising taxes on the rich, the idea of imposing such increases might be difficult, especially after the recent tax hikes in this year’s state budget.

“The first thing I would tell you is that I would look forward to negotiating and finalizing this bill with Governor Hochul,” Rivera says, citing his and colleagues’ calls for Governor Cuomo’s impeachment after several sexual assault allegations and the administration’s botched handling of COVID nursing home cases last year. Gottfried’s camp defends the income and payroll tax rates as fair and necessary to avoiding a snafu like Vermont’s Green Mountain Care, that state’s shot at single-payer which fell dead in the water in 2014 largely because of a flat tax rate that would have placed an undue burden on middle- and low-income residents. He shrugs off fears of the rich fleeing the state if more taxes are imposed, insisting that New York’s tax record refutes that. The elimination of costs shifted onto the insured by providers looking to recoup losses from treating the uninsured would work to drive down costs for all, Gottfried says.

The alternatives offered by critics of the NYHA are more or less business as usual. Politi points to New York’s Health Care Administrative Simplification Workgroup—a working group formed in October 2020 made up of insurers, providers, and consumer groups—as a model for how more public-private partnerships could tackle problems like the state’s hidden taxes on private insurance that increase premiums 6 to 9 percent.

One thing both sides agree on is that a half-measure like a government-run public option that people could buy into if they wanted isn’t the answer. For the skeptics, a public option is just a slippery slope to single-payer, while NYHA adherents worry it would be too costly and undermine the savings they are setting their sights on.

Likewise, the Biden administration’s current strategy of expanding on provisions within the ACA, Medicaid, and COBRA will likely help more than 5 million Americans obtain and retain some level of health coverage, but the future sticker price for maintaining such a highly regulated market will skyrocket. The extra $20 billion in subsidies for qualified ACA marketplace plans amounts to taxpayers doling out more than $8,500 for every American on a subsidized plan next year, about 40 percent more than in 2020, according to data from the Congressional Budget Office.

For NYHA’s acolytes, its passage is as much about preventing a looming crisis as it is correcting past mistakes. Despite the robust vaccine rollout foreshadowing a return to work, school, and travel, we’re still a long way off from a pre-COVID normal. Active coronavirus cases continue to rise across the country—even in New York State, where new infections abound—and more than 10 million Americans remain out of work. While the combination of third-round stimulus checks, extended unemployment benefits, and continued pauses on student loans, mortgages, and evictions have been effective holdovers, the jury is still out on whether the worst is yet to come once those moratoriums expire.

Vangas was able to put off her mortgage payments initially, but that assistance became irrelevant once she and her fiancé split. Altogether she’s seen little in the way of help from either the state or federal government.

“Obviously the stimulus checks went out to everyone, but that’s honestly not that helpful when you’ve been out of work for a year,” she says. “Like, $1,200 doesn’t go very far.”

Vangas tries to take it all in stride, but the glaring lack of help afforded to long COVID sufferers feels disheartening, to say the least. “I think that [the government] absolutely should be helping, especially since they don’t give us any information on what’s going on,” she says. “We’re fighting for our lives. I think more can be done if they wanted it to be done.”